Free Annual Internal Audit Accounting Strategy Plan

Executive Summary

The Annual Internal Audit Accounting Strategy Plan is a pivotal initiative designed to fortify the internal audit framework, thereby elevating the efficiency of financial management and reinforcing accountability and overarching control mechanisms within the organization. This strategic plan is crafted with the intent to embed a culture of transparency and to proactively identify and mitigate potential risks that could undermine the financial stability and integrity of the organization.

At the heart of this strategy is the commitment to uphold the highest standards of financial governance, ensuring that every financial transaction and decision aligns with the organization's core values and regulatory requirements. By implementing cutting-edge audit methodologies and leveraging advanced analytical tools, the plan aims to provide a comprehensive overview of the financial landscape, highlighting areas of excellence and pinpointing opportunities for enhancement.

The strategic plan encompasses a broad spectrum of activities, from the meticulous review of financial statements to the rigorous assessment of internal controls and compliance mechanisms. It is structured to not only safeguard the organization's assets but also to foster an environment that encourages prudent financial management, operational efficiency, and strategic decision-making. Through this holistic approach, the plan aspires to contribute significantly to the organization's long-term success and sustainability.

Objectives of the Audit

The objectives of the Annual Internal Audit are multifaceted and are designed to provide a thorough examination of the organization's financial operations, ensuring they meet the highest standards of integrity and compliance. The primary goals of the audit are as follows:

Statutory Compliance: The audit rigorously evaluates the organization's adherence to legal and regulatory frameworks, ensuring that all financial activities are conducted in accordance with the pertinent statutes and guidelines. This includes examining the organization's compliance with tax laws, financial reporting standards, and any other relevant legal obligations. The objective is to preemptively identify and rectify any deviations from statutory requirements, thereby minimizing the risk of legal sanctions and reputational damage.

Financial System Soundness: A critical component of the audit involves assessing the robustness of the financial system. This encompasses an evaluation of the accounting practices, financial controls, and reporting mechanisms in place. The aim is to ascertain the reliability and accuracy of financial information, which is pivotal for informed decision-making and effective financial management.

Risk Assessment: The audit undertakes a comprehensive analysis of business risks, encompassing both internal vulnerabilities and external threats. This involves identifying potential risk factors that could adversely affect the organization's financial health, operational continuity, or strategic objectives. The audit seeks to provide actionable insights and recommendations for mitigating these risks, thereby enhancing the organization's resilience and adaptability.

Loophole Identification: An integral part of the audit is the detection of loopholes or weaknesses within the financial system that could be exploited or lead to inefficiencies. This includes scrutinizing the internal control mechanisms and identifying areas where the system is susceptible to fraud, errors, or mismanagement. By addressing these vulnerabilities, the audit aims to strengthen the organization's financial infrastructure and safeguard its assets.

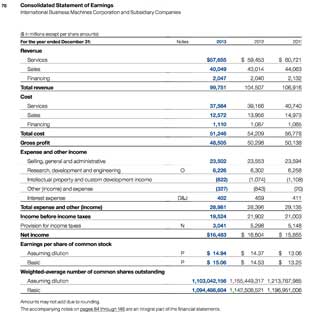

Financial Statement

Fig 1: Example of a Company's Annual Financial Statement

The review of financial statements stands as the cornerstone of the Annual Internal Audit, offering a transparent and accurate reflection of the organization's financial activities over the preceding year. This meticulous examination encompasses the following key components:

Balance Sheet Analysis: A thorough analysis of the balance sheet provides insights into the organization's financial position at the end of the fiscal year. This includes assessing the accuracy of recorded assets, liabilities, and equity, ensuring that they accurately reflect the organization's financial reality. The audit scrutinizes the valuation methodologies applied to assets and liabilities, verifying their compliance with accepted accounting principles and standards.

Income Statement Review: The review of the income statement, or profit and loss statement, focuses on evaluating the organization's financial performance over the fiscal period. This involves analyzing revenue streams, expenditure patterns, and profitability indicators. The audit aims to verify the accuracy and completeness of income and expense records, ensuring they are appropriately categorized and recorded.

Cash Flow Statement Examination: An examination of the cash flow statement is critical to understanding the liquidity and solvency of the organization. The audit assesses the sources and uses of cash, ensuring that cash flows from operating, investing, and financing activities are accurately reported and reflect the organization's cash management practices.

Notes and Disclosures: The audit also pays close attention to the notes and disclosures accompanying the financial statements. These provide essential context and details regarding the accounting policies, assumptions, and estimates used in preparing the financial statements. The audit evaluates the adequacy and transparency of these disclosures, ensuring they provide a comprehensive understanding of the financial statements.

Through this comprehensive review, the Annual Internal Audit endeavors to affirm the integrity and transparency of the financial statements, providing stakeholders with confidence in the organization's financial health and management practices. This rigorous examination lays the groundwork for identifying areas for improvement, enhancing financial controls, and fostering a culture of continuous improvement within the organization.

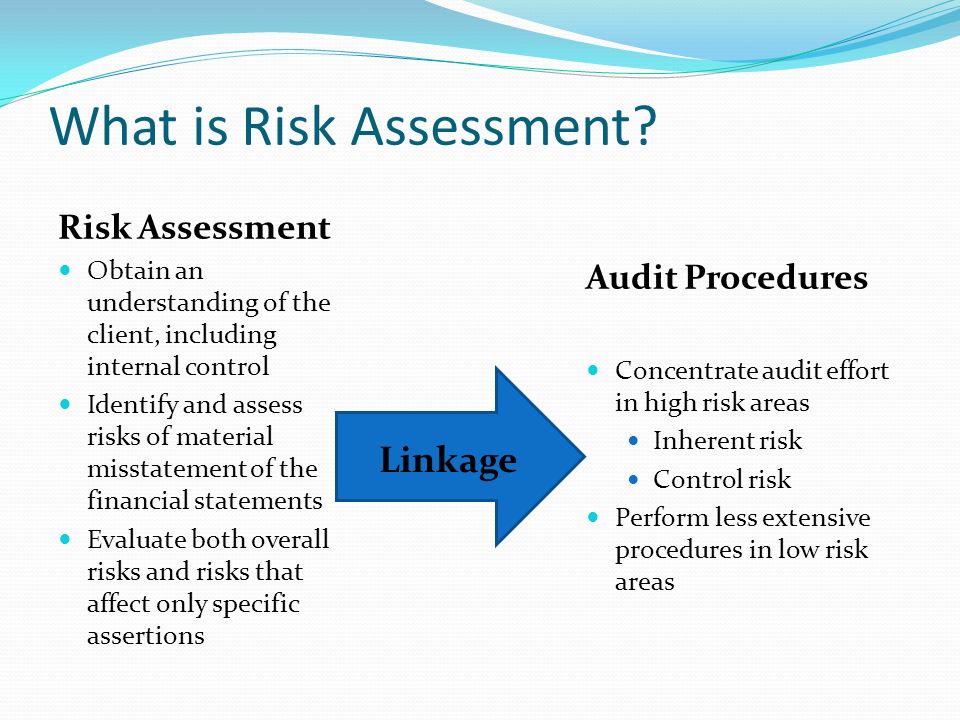

Comprehensive Risk Assessment

Fig 2: Infographic of a Company Internal Audit Accounting Risk Assessment

The Comprehensive Risk Assessment segment of the Annual Internal Audit Accounting Strategy Plan is a critical component designed to proactively identify, evaluate, and mitigate potential threats that could compromise the organization's financial integrity and overall operational resilience. This meticulous process encompasses a wide array of risk factors, both internal and external, that could pose significant challenges to the organization.

Internal Systems Review: The audit begins with an in-depth examination of the organization's internal systems, focusing on financial processes, internal controls, IT infrastructure, and human resources. This review aims to uncover any inherent weaknesses or inefficiencies that might make the organization susceptible to financial errors, fraud, and mismanagement. By identifying these vulnerabilities early, the organization can implement corrective measures to fortify its internal systems and safeguard its financial assets.

External Threat Analysis: In addition to internal vulnerabilities, the risk assessment also considers a variety of external threats that could impact the organization's financial stability. This includes:

Market Volatility: The audit evaluates the organization's exposure to market fluctuations, including interest rate changes, currency exchange rate movements, and commodity price variations. Understanding these factors is crucial for developing effective risk management strategies to mitigate potential financial losses.

Regulatory Changes: With the ever-evolving regulatory landscape, the audit assesses the organization's readiness to adapt to new financial norms, laws, and regulations. This involves analyzing the potential impact of forthcoming regulatory changes on the organization's operations and financial reporting practices.

Industry Trends: The audit also considers broader industry trends that could affect the organization's competitive position and financial performance. This includes technological advancements, shifts in consumer behavior, and emerging market opportunities and threats.

By conducting a comprehensive risk assessment, the organization can develop a strategic approach to risk management, prioritizing high-impact risks and implementing targeted mitigation strategies to enhance its financial resilience and operational stability.

Evaluation of Internal Controls

The Evaluation of Internal Controls is a cornerstone of the Annual Internal Audit, focusing on scrutinizing the effectiveness and robustness of the organization's existing internal control mechanisms. This evaluation is pivotal in identifying any inefficiencies, vulnerabilities, and areas ripe for enhancement within the control environment.

Control Environment Assessment: The audit delves into the overarching control environment, examining the organizational structure, ethical values, and the overall attitude of management and employees towards internal control and risk management. This includes assessing the tone at the top, which sets the cultural foundation for internal controls.

Control Activities Review: The audit systematically reviews control activities across various departments and processes, including authorization procedures, verification processes, reconciliation practices, and access controls to sensitive information and assets. This review aims to ensure that control activities are appropriately designed and effectively implemented to prevent and detect errors, fraud, and non-compliance with policies and regulations.

Information and Communication Systems Analysis: The audit evaluates the effectiveness of the organization's information systems and communication channels in capturing, processing, and disseminating financial and operational information. This includes reviewing the reliability of IT systems in maintaining data integrity, the adequacy of financial reporting mechanisms, and the effectiveness of communication protocols in ensuring that relevant information reaches the appropriate personnel in a timely manner.

Monitoring Activities Evaluation: Continuous monitoring of internal controls is essential for their effectiveness. The audit assesses the organization's monitoring activities, including regular management and supervisory reviews, internal audit functions, and external audits. This evaluation seeks to ensure that monitoring mechanisms are in place to identify and address any deficiencies in internal controls promptly.

Through a thorough evaluation of internal controls, the audit aims to identify potential improvements that could enhance the organization's ability to prevent financial mishaps, ensure the accuracy of financial data, and maintain operational efficiency.

Review of Regulatory Compliance

The Review of Regulatory Compliance is an essential element of the Annual Internal Audit, designed to ensure that the organization's financial practices and procedures adhere to the required financial norms, laws, and regulations. This review serves as a safeguard against legal liabilities and reputational damage that could arise from non-compliance.

Compliance Framework Assessment: The audit begins with an assessment of the organization's compliance framework, examining the policies, procedures, and controls in place to ensure regulatory compliance. This includes reviewing the organization's understanding of applicable laws and regulations and its capacity to stay abreast of regulatory changes.

Specific Regulatory Requirements Review: The audit conducts a detailed review of compliance with specific regulatory requirements relevant to the organization's operations. This encompasses tax laws, financial reporting standards, data protection regulations, and any industry-specific regulations. The objective is to identify any areas of non-compliance and recommend corrective actions to address these issues.

Regulatory Change Readiness: In a rapidly changing regulatory environment, the audit evaluates the organization's readiness to adapt to new regulatory requirements. This involves assessing the processes and systems in place for monitoring regulatory developments and implementing necessary changes to policies, procedures, and controls in response to new regulatory demands.

Compliance Training and Awareness: The audit also examines the organization's efforts to promote compliance awareness and understanding among its employees. This includes evaluating the effectiveness of training programs, communication of compliance policies, and the establishment of a compliance culture within the organization.

By conducting a comprehensive review of regulatory compliance, the audit aims to ensure that the organization not only meets current regulatory requirements but is also well-prepared to adapt to future changes in the regulatory landscape. This proactive approach to regulatory compliance helps to protect the organization from potential legal and financial penalties and supports its long-term sustainability and success.

Supply Chain Assessment

The Supply Chain Assessment within the Annual Internal Audit Accounting Strategy Plan is a vital examination tailored to businesses with integral supply chain operations. This assessment delves into the intricacies of supply chain processes, from procurement and production to distribution and customer delivery. The primary aim is to ensure the financial transparency of the company's interactions with suppliers and clients, thereby safeguarding against inefficiencies, fraud, and financial mismanagement that could compromise the organization's integrity and profitability.

Procurement and Vendor Management: The audit scrutinizes the procurement policies and practices, assessing the methods used for vendor selection, contract negotiation, and performance evaluation. This includes evaluating the fairness and transparency of procurement processes, the effectiveness of cost control measures, and the robustness of vendor risk management practices.

Inventory Management and Controls: An in-depth review of inventory management practices is conducted to ensure that inventory levels are optimized, costs are accurately recorded, and losses due to waste, theft, or obsolescence are minimized. The audit examines inventory valuation methods, stock rotation procedures, and the effectiveness of inventory control systems.

Production and Cost Analysis: For organizations involved in manufacturing, the audit assesses production processes to ensure that costs are accurately captured and allocated. This includes evaluating the efficiency of production operations, the accuracy of cost accounting methods, and the effectiveness of cost management strategies.

Distribution and Logistics: The audit reviews the distribution and logistics operations, focusing on the efficiency and reliability of the supply chain network. This includes assessing the cost-effectiveness of transportation modes, the reliability of delivery schedules, and the adequacy of logistics controls.

Supplier and Client Financial Transactions: A critical component of the supply chain assessment is the review of financial transactions with suppliers and clients. The audit verifies the accuracy and completeness of these transactions, ensuring that payments are properly authorized, recorded, and reconciled.

Through the Supply Chain Assessment, the audit aims to identify potential risks and inefficiencies within the supply chain, providing recommendations for enhancing financial transparency, improving operational efficiency, and strengthening supplier and client relationships.

Tax Compliance

The Tax Compliance review is a cornerstone of the Annual Internal Audit, emphasizing the importance of adhering to tax laws and regulations to avoid significant financial penalties and legal repercussions. This comprehensive review covers various aspects of tax compliance, from the accuracy of tax filings to the appropriateness of tax deductions and the management of employee benefit plans.

Tax Filings and Payments: The audit meticulously examines the organization's tax filings, ensuring that all required tax returns are accurately prepared and filed timely with the relevant tax authorities. This includes verifying the correctness of income, sales, payroll, and other applicable taxes, and ensuring that tax payments are made in accordance with statutory deadlines.

Tax Deductions and Credits: The review assesses the validity and appropriateness of tax deductions and credits claimed by the organization. This involves scrutinizing the documentation and justification for deductions, such as business expenses, depreciation, and tax credits, to ensure they comply with tax laws and regulations.

Employee Benefit Plans and Payroll Taxes: The audit evaluates the organization's compliance with tax requirements related to employee benefit plans and payroll taxes. This includes reviewing the treatment of employee compensations, benefits, and contributions to retirement plans, ensuring that all payroll tax obligations are accurately calculated and remitted.

Tax Risk Management: The audit also assesses the organization's tax risk management practices, evaluating the processes in place for identifying, assessing, and mitigating tax-related risks. This includes reviewing the organization's readiness to adapt to changes in tax laws and the effectiveness of tax planning strategies.

By conducting a thorough Tax Compliance review, the audit aims to ensure that the organization maintains a strong compliance posture, minimizing the risk of tax-related issues and contributing to the organization's overall financial health and stability.

The Audit Report

The culmination of the Annual Internal Audit Accounting Strategy Plan is the presentation of The Audit Report. This comprehensive document encapsulates the findings, insights, and recommendations derived from the audit process, providing a holistic view of the organization's financial standing, operational efficiencies, and potential risks.

Financial Standing Overview: The report begins with an overview of the organization's current financial position, summarizing key financial metrics such as revenue, profit margins, liquidity ratios, and capital structure. This section provides stakeholders with a clear snapshot of the organization's financial health.

Operational Efficiencies and Inefficiencies: The report details the operational efficiencies identified during the audit, highlighting areas where the organization excels. Conversely, it also points out inefficiencies and areas of concern, providing a balanced view of operational performance.

Risk Assessment Findings: A significant portion of the report is dedicated to the findings from the comprehensive risk assessment. This includes a detailed analysis of internal and external risks, their potential impact on the organization, and the effectiveness of existing risk management strategies.

Recommendations for Improvement: The core of the report is the recommendations section, where actionable insights for enhancing financial systems, internal controls, compliance, and overall operational efficiency are presented. These recommendations are prioritized based on their potential impact and feasibility of implementation.

Implementation and Follow-up: The report concludes with a proposed plan for implementing the audit recommendations, including timelines, responsible parties, and monitoring mechanisms. This ensures that the audit findings are translated into concrete actions that contribute to the organization's continuous improvement and success.

The Audit Report serves as a valuable tool for management, providing them with the insights needed to make informed decisions, address potential vulnerabilities, and steer the organization towards sustainable growth and prosperity.

Audit Follow-up

In order to actualize change, it is important for audit findings to be implemented. A follow-up ensures that the audit is taken seriously and that the management acts upon the recommendations intended to increase financial efficiency and mitigate risks.

- 100% Customizable, free editor

- Access 1 Million+ Templates, photo’s & graphics

- Download or share as a template

- Click and replace photos, graphics, text, backgrounds

- Resize, crop, AI write & more

- Access advanced editor

Template.net's Annual Internal Audit Accounting Strategy Plan Template, meticulously crafted for your convenience, offers a comprehensive solution for businesses. With editable features powered by our AI editor tool, streamline your audit strategy effortlessly. This template ensures precision and efficiency in your financial operations, making it an essential asset for every organization's success.

You may also like

- Finance Plan

- Construction Plan

- Sales Plan

- Development Plan

- Career Plan

- Budget Plan

- HR Plan

- Education Plan

- Transition Plan

- Work Plan

- Training Plan

- Communication Plan

- Operation Plan

- Health And Safety Plan

- Strategy Plan

- Professional Development Plan

- Advertising Plan

- Risk Management Plan

- Restaurant Plan

- School Plan

- Nursing Home Patient Care Plan

- Nursing Care Plan

- Plan Event

- Startup Plan

- Social Media Plan

- Staffing Plan

- Annual Plan

- Content Plan

- Payment Plan

- Implementation Plan

- Hotel Plan

- Workout Plan

- Accounting Plan

- Campaign Plan

- Essay Plan

- 30 60 90 Day Plan

- Research Plan

- Recruitment Plan

- 90 Day Plan

- Quarterly Plan

- Emergency Plan

- 5 Year Plan

- Gym Plan

- Personal Plan

- IT and Software Plan

- Treatment Plan

- Real Estate Plan

- Law Firm Plan

- Healthcare Plan

- Improvement Plan

- Media Plan

- 5 Year Business Plan

- Learning Plan

- Marketing Campaign Plan

- Travel Agency Plan

- Cleaning Services Plan

- Interior Design Plan

- Performance Plan

- PR Plan

- Birth Plan

- Life Plan

- SEO Plan

- Disaster Recovery Plan

- Continuity Plan

- Launch Plan

- Legal Plan

- Behavior Plan

- Performance Improvement Plan

- Salon Plan

- Security Plan

- Security Management Plan

- Employee Development Plan

- Quality Plan

- Service Improvement Plan

- Growth Plan

- Incident Response Plan

- Basketball Plan

- Emergency Action Plan

- Product Launch Plan

- Spa Plan

- Employee Training Plan

- Data Analysis Plan

- Employee Action Plan

- Territory Plan

- Audit Plan

- Classroom Plan

- Activity Plan

- Parenting Plan

- Care Plan

- Project Execution Plan

- Exercise Plan

- Internship Plan

- Software Development Plan

- Continuous Improvement Plan

- Leave Plan

- 90 Day Sales Plan

- Advertising Agency Plan

- Employee Transition Plan

- Smart Action Plan

- Workplace Safety Plan

- Behavior Change Plan

- Contingency Plan

- Continuity of Operations Plan

- Health Plan

- Quality Control Plan

- Self Plan

- Sports Development Plan

- Change Management Plan

- Ecommerce Plan

- Personal Financial Plan

- Process Improvement Plan

- 30-60-90 Day Sales Plan

- Crisis Management Plan

- Engagement Plan

- Execution Plan

- Pandemic Plan

- Quality Assurance Plan

- Service Continuity Plan

- Agile Project Plan

- Fundraising Plan

- Job Transition Plan

- Asset Maintenance Plan

- Maintenance Plan

- Software Test Plan

- Staff Training and Development Plan

- 3 Year Plan

- Brand Activation Plan

- Release Plan

- Resource Plan

- Risk Mitigation Plan

- Teacher Plan

- 30 60 90 Day Plan for New Manager

- Food Safety Plan

- Food Truck Plan

- Hiring Plan

- Quality Management Plan

- Wellness Plan

- Behavior Intervention Plan

- Bonus Plan

- Investment Plan

- Maternity Leave Plan

- Pandemic Response Plan

- Succession Planning

- Coaching Plan

- Configuration Management Plan

- Remote Work Plan

- Self Care Plan

- Teaching Plan

- 100-Day Plan

- HACCP Plan

- Student Plan

- Sustainability Plan

- 30 60 90 Day Plan for Interview

- Access Plan

- Site Specific Safety Plan